The Seven-Second Miracle: How Your Card Actually Pays for That Coffee

Tracing the invisible infrastructure that makes a two-second card tap possible across the globe.

A scene you've lived a thousand times

You're at a counter. You tap your card. The machine blinks. Two seconds later, beep: "approved." You walk out with your coffee.

In those two seconds, five organisations that have never met, don't inherently trust each other, and are scattered across different cities, sometimes different countries, just had a conversation, made a decision, and shook hands on your behalf. You didn't see any of it. That's the whole point. Good infrastructure is invisible.

This piece is about making that infrastructure visible. We're going to walk through it exactly in the order it actually happens, not topic by topic, but moment by moment, the way it really unfolds. By the end, you'll understand it whether you've never written a line of code, or whether you're the one building the next layer on top of it.

The card is not money. It's a passport.

Start here, because everything else only makes sense once this clicks.

Your card doesn't hold money. It never did. Think of it instead like a passport: it doesn't contain your identity, it proves your identity to whoever's checking. A passport gets you through immigration; a card gets your bank to say "yes, this person is who they claim to be, and yes, they're good for this amount."

Look at the numbers on the card and they stop being random.

The BIN: The first 6 to 8 digits are like a passport's country code, they instantly tell any system in the world which bank issued this card and which network it belongs to (Visa, Mastercard, RuPay). This little sequence is called the Bank Identification Number, and it's the very first thing read the moment your card touches a machine.

The CVV: This is like a security stamp only visible when you physically hold the passport, proof you're not just reciting a number you memorised off someone else's card.

The Chip: This is the clever part. Old magnetic stripe cards said the same fixed thing every single time, easy to copy, like a photocopied ID. The chip instead generates a brand new, one-time code for every single transaction. Even if someone recorded today's code, it's useless tomorrow.

So the coffee shop machine isn't reading "money." It's reading a passport and asking a question: can this person's home bank vouch for them, right now, for this amount? That question is about to travel much further than you'd guess.

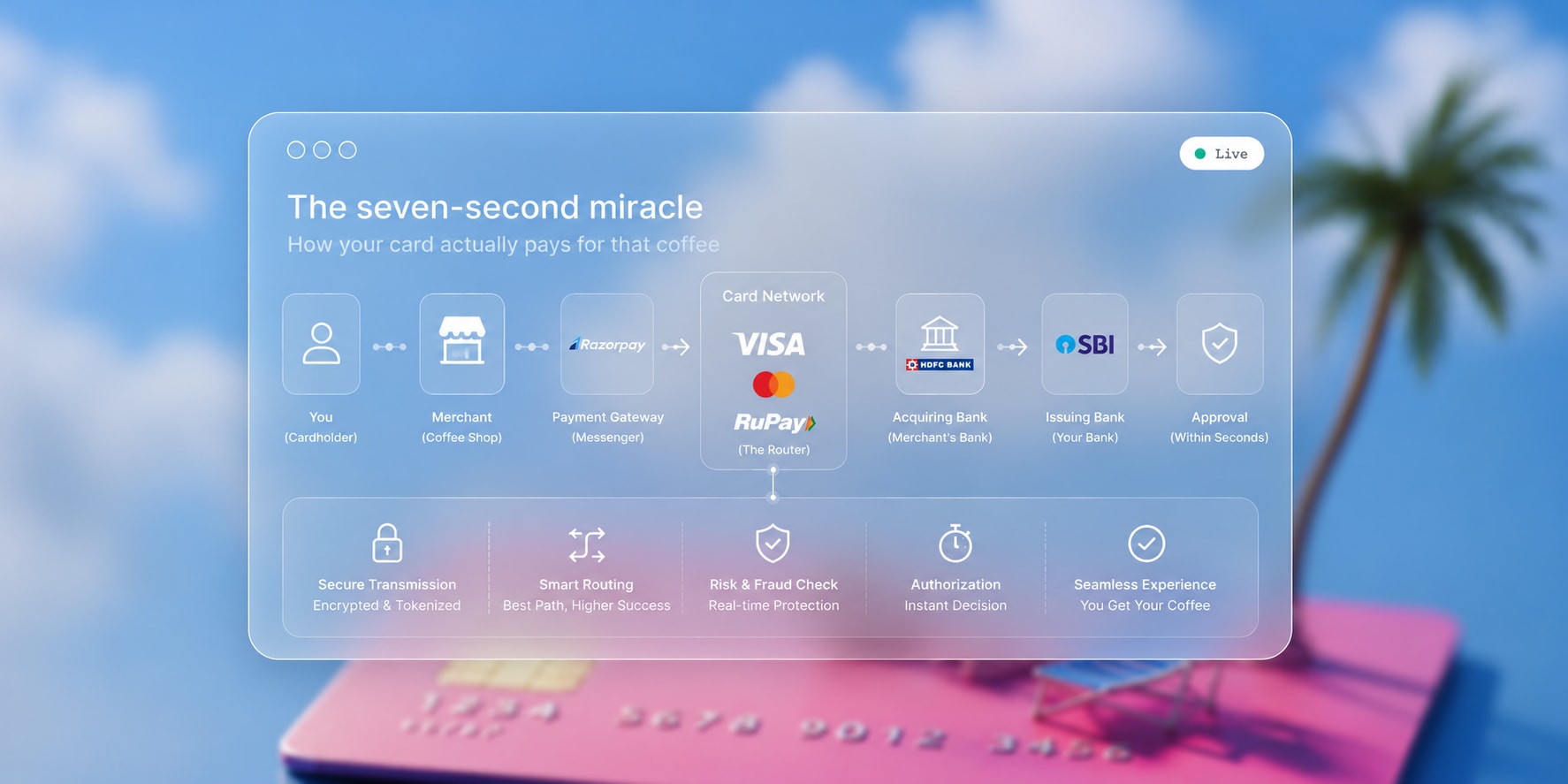

The four strangers who have to agree

For your two-second tap to work, four separate parties (who have never spoken to each other before this exact moment) need to fall in line, instantly, in order:

1. You (the cardholder), asking to spend.

2. The coffee shop (the merchant), asking to get paid.

3. The coffee shop's bank (the acquirer), the shop's own banking partner, whose job is to "acquire" this sale on the shop's behalf.

4. Your bank (the issuer), the one that actually issued you the card, and the only party on this list who can say yes or no, because it's the only one who can see your actual balance.

And sitting in the middle, connecting all four, is a fifth party who owns none of the money and touches none of it directly: the card network (Visa, Mastercard, or RuPay). Think of the network less like a bank and more like an air traffic control tower. It doesn't fly the planes (move the money), it makes sure every plane (every transaction) gets routed to the right runway (the right issuing bank) without chaos.

Nobody in this list is a "payment gateway" yet. That's the sixth character, and it enters right at the very first step, because someone has to actually carry your card details from the checkout screen to this whole system in the first place.

The messenger: what a payment gateway actually does

Here's where Razorpay, Cashfree, and Stripe enter the story. And here's the biggest misconception to clear up immediately: a payment gateway does not hold or move your money. Not even for a second.

What it actually does is closer to a diplomatic translator and courier, sitting between you and that four-party dance:

It captures your card details on a checkout page, in a way designed so the shop's own website never actually sees your real card number, it goes straight into a secure vault.

It immediately disguises that card number into a meaningless reference code (a token), so even if someone intercepted it, they'd get nothing usable.

It then speaks, on the merchant's behalf, in a very old, very rigid language that every bank on earth still understands, carrying the request from the merchant's side all the way to the network.

And this part is genuinely clever: if the transaction fails for a technical reason, a good gateway will silently try re-routing it through a different partner bank before you even notice the first attempt didn't go through. This is called intelligent routing, and it's one of the few places gateways actually compete on real technical merit, not just price.

So think of the gateway as the courier who runs your passport (the card) from the checkout counter to immigration (your bank), speaks fluent bureaucrat, and brings the stamped answer back, all in about two seconds.

The two-second lie (and why it's actually fine)

Here's the twist almost nobody outside the industry knows, and it's the single most important idea in this whole piece:

When you see "Payment Successful," no money has moved yet.

What actually happened is that your bank looked at the request, said "yes, I vouch for this, I'll pay," and put a hold on that amount in your account, like a bank teller saying "consider it done" and putting a sticky note on your file, rather than physically walking cash to the other bank right then.

The real movement of money, actual funds leaving your bank's vault and landing in the coffee shop's bank's vault, happens later, usually bundled up with thousands of other transactions from that day, and settled as one batch, typically a day or two later. This two-step dance has names: the instant "yes, I'll pay" is called authorization; the actual money changing hands afterward is called clearing and settlement.

This is exactly why some payment platforms sell "instant settlement" as a premium feature. They're not doing anything magical, they're just fronting you your own money a day early, before they themselves have received it from the bank side of things.

So: the coffee shop got a promise, instantly. They get the actual rupees, a day or two later. Both are true and both are normal. The system works precisely because everyone trusts that promise enough to hand over a coffee before the cash physically arrives.

The secret language every bank still speaks

Now the part that feels like genuine magic once you see it.

How does a two-second conversation actually travel reliably between a checkout page in Amaravati, a bank in Mumbai, a network switch somewhere else entirely, and finally an issuing bank's core system, and get a definitive yes/no answer back before your coffee gets cold?

The answer is a messaging format from the 1980s, called ISO 8583, and it is, almost unbelievably, still running underneath nearly every card transaction on the planet today.

Picture it like a very strict, very old telegram format. Every message has:

A short code at the top saying what kind of message this is: "this is a request to authorize a payment," or "this is the response to that request." Technically, a 4-digit MTI (Message Type Indicator).

A checklist telling the receiving computer exactly which pieces of information are attached in this particular telegram (a bitmap).

Then the actual fields: the card number, the amount, the merchant's category, and so on.

And when your bank approves or declines you, it isn't sending back a friendly sentence, it's sending back a tiny numeric code. `00` means approved. `51` means insufficient funds. `05` means a flat "do not honor." Every "Your payment failed, please try again" message you've ever seen on a checkout page is a payment gateway quietly translating one of these blunt, decades-old codes into something a human can read without panicking.

It's a strange thing to sit with: some of the most modern-feeling technology you use every day, tapping a phone to pay for coffee, is, underneath several layers of polish, still speaking a dialect invented before most of us were born.

The invisible tollbooth: where the fee actually goes

Every card payment costs something, usually 1 to 3% of the transaction, called the MDR (Merchant Discount Rate). It feels like the gateway is charging this. It isn't, not entirely. That fee gets split three ways, like a toll being divided between three different agencies that all maintained a piece of the road you just drove on:

A slice goes to your bank, the issuer, because they're the one who actually took the risk of vouching for you.

A slice goes to the network (Visa/Mastercard/RuPay), for running the switchboard that connected everyone.

The remaining slice is what the gateway and the merchant's bank actually keep, for the courier work, the security, the fraud checks, and everything from the gateway layer.

So next time a fee looks high, remember: it's not one company's markup, it's three different tolls stacked on top of each other, and the gateway is usually the smallest of the three.

The safety nets underneath everything

A few more characters show up here, quietly, in every transaction, doing work you never see:

PCI-DSS is the industry's shared rulebook for handling card data safely: no storing CVVs after the fact, everything encrypted, strict access controls. Any company touching card numbers has to follow it.

OTPs and 3D Secure are the extra knock on the door, a second layer of proof beyond the card itself, mandatory in India, which is exactly why you get that OTP popup on Indian cards but sometimes not on foreign ones.

Tokenization means merchants aren't even allowed to keep your real card number stored anymore, only a meaningless substitute token that's useless to anyone who steals it.

None of this is decoration. Every one of these exists because, at some point in payment history, its absence caused real damage to real people, and the system adapted.

When the story goes backward

Sometimes, after all of this, the customer says: that wasn't me, or I never got what I paid for.

This triggers a chargeback. The entire flow essentially runs in reverse. The issuing bank pulls the money back, the network processes the dispute, and the merchant (often with the gateway's help gathering evidence like delivery proof, chat logs, receipts) has to make their case or lose the money, sometimes with an extra penalty on top. It's one of the least talked-about, most operationally painful parts of running any business that takes card payments online, and one of the real reasons gateways earn their fee.

Same play, different actors

Cashfree, Razorpay, and Stripe are all playing the exact role of courier, translator, and risk-checker. What differs is the terrain they operate on.

Stripe grew up in markets where cards and bank transfers (ACH) dominate, so its deepest muscles are in card tokenization and subscription billing. Razorpay and Cashfree grew up in India, where UPI (not cards) carries most of the daily volume, so their deepest muscles are in RBI compliance, escrow account management, and NPCI integration. Same job description, different terrain, different scar tissue.

The whole journey, in one breath

A card is a passport, not a wallet. A payment gateway is the courier that carries that passport's proof to the right immigration desk without ever peeking inside it. The "approved" you see in two seconds is a promise, not a payment: the real money follows a day or two later, in a batch, through a decades-old telegram language that somehow still runs the modern world. Every fee along the way is a toll shared between three different guardians of that journey, and a scaffolding of rules quietly stands underneath all of it so that a stranger's "yes" is actually worth trusting.

That's the seven-second miracle. It happens every time you tap.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, legal, or professional advice. Orite does not guarantee the accuracy, completeness, or timeliness of the information provided.